Affordability meets debt: Americans are using credit cards to pay for everyday life

Americans relying more on credit cards while interest rates and delinquencies climb

I took the dog into the groomer’s last week and Heidi chatted me up as she prepared Beau for his beauty treatment.

“I just can’t save any money this year. I try hard, I keep track of everything and try to stick to a budget but I’m way behind last year. And that was worse than the year before that,” she said. “Thanks for the tip last time, by the way, Mr. Hood. I really appreciate it.”

I was impressed with Heidi’s diligence and with her social skills. She not only remembered my name but remembered the tip and reminded me of it in a nice way, smoothing the way for a repeat.

But while Heidi is doing everything right, at least as far as I could tell, she is in the same spot as millions of Americans — facing rising costs and stagnant or nearly stagnant earnings tinged by the fear that AI, inflation, recession or some other mega force may push her even farther down the affordability ladder.

This chronic shortfall of income versus expense is driving ever larger numbers of consumers towards debt — relying on credit cards and other forms of borrowing to cover basic expenses, a trend that economists say highlights the widening gap between household budgets and the price of necessities.

Recent data from the Federal Reserve Bank of New York shows credit card balances remain near record highs, while interest rates and delinquency rates are also rising. Together, the trends paint a picture of consumers who are leaning more heavily on debt to manage the cost of groceries, housing, utilities, and health care.

The shift raises a key question for policymakers and consumer advocates: How sustainable is the growing reliance on credit to maintain everyday living standards?

Credit card balances remain elevated

According to the latest Household Debt and Credit Report from the Federal Reserve Bank of New York, Americans now carry well over $1 trillion in credit card debt, a level that surged following the pandemic-era inflation spike.

Balances increased steadily through 2022 and 2023 as prices for food, rent, and energy climbed faster than many workers’ wages. While the pace of growth has slowed somewhat in recent quarters, total balances remain historically high.

Economists say the pattern suggests many households are using credit cards less for discretionary purchases and more for routine expenses.

“Credit cards are increasingly functioning as a financial bridge,” analysts noted in the report, helping families cover costs between paychecks or deal with sudden expenses.

Interest rates add to the pressure

At the same time that Americans are carrying more credit card debt, the cost of borrowing has also increased sharply.

Average credit card annual percentage rates (APRs) are now among the highest in decades, often exceeding 20 percent, according to industry tracking data.

Those rates rose rapidly after the Federal Reserve System increased benchmark interest rates to combat inflation. Because most credit cards carry variable rates tied to those benchmarks, the hikes quickly translated into higher borrowing costs for consumers.

The result: balances that might once have been manageable can now grow quickly due to interest charges.

Consumer advocates warn this dynamic can trap borrowers in a cycle where minimum payments primarily cover interest rather than reducing the principal balance.

Delinquencies begin to rise

Another indicator drawing attention from economists is the increase in delinquency rates, particularly among younger borrowers.

The Federal Reserve Bank of New York report shows that the share of credit card balances transitioning into delinquency — meaning payments are at least 30 days late — has climbed over the past year.

While delinquency levels remain below the peaks seen during the 2008 financial crisis, the upward trend has raised concerns about the financial resilience of many households.

Young borrowers and lower-income households appear to be facing the greatest stress.

Many of these consumers entered the pandemic with relatively little debt but are now encountering higher living costs combined with rising borrowing costs.

Everyday expenses are driving borrowing

The increased reliance on credit cards reflects a broader affordability challenge affecting large segments of the population.

Several major spending categories have seen particularly steep price increases in recent years, including:

groceries

rent and housing costs

insurance premiums

utility bills

medical expenses

For households whose incomes have not kept pace with inflation, credit cards have become a common tool to smooth out financial pressure.

In surveys conducted by consumer research groups, many respondents report using credit cards for expenses they previously paid with cash or debit.

Some also say they are carrying balances longer than they did in the past.

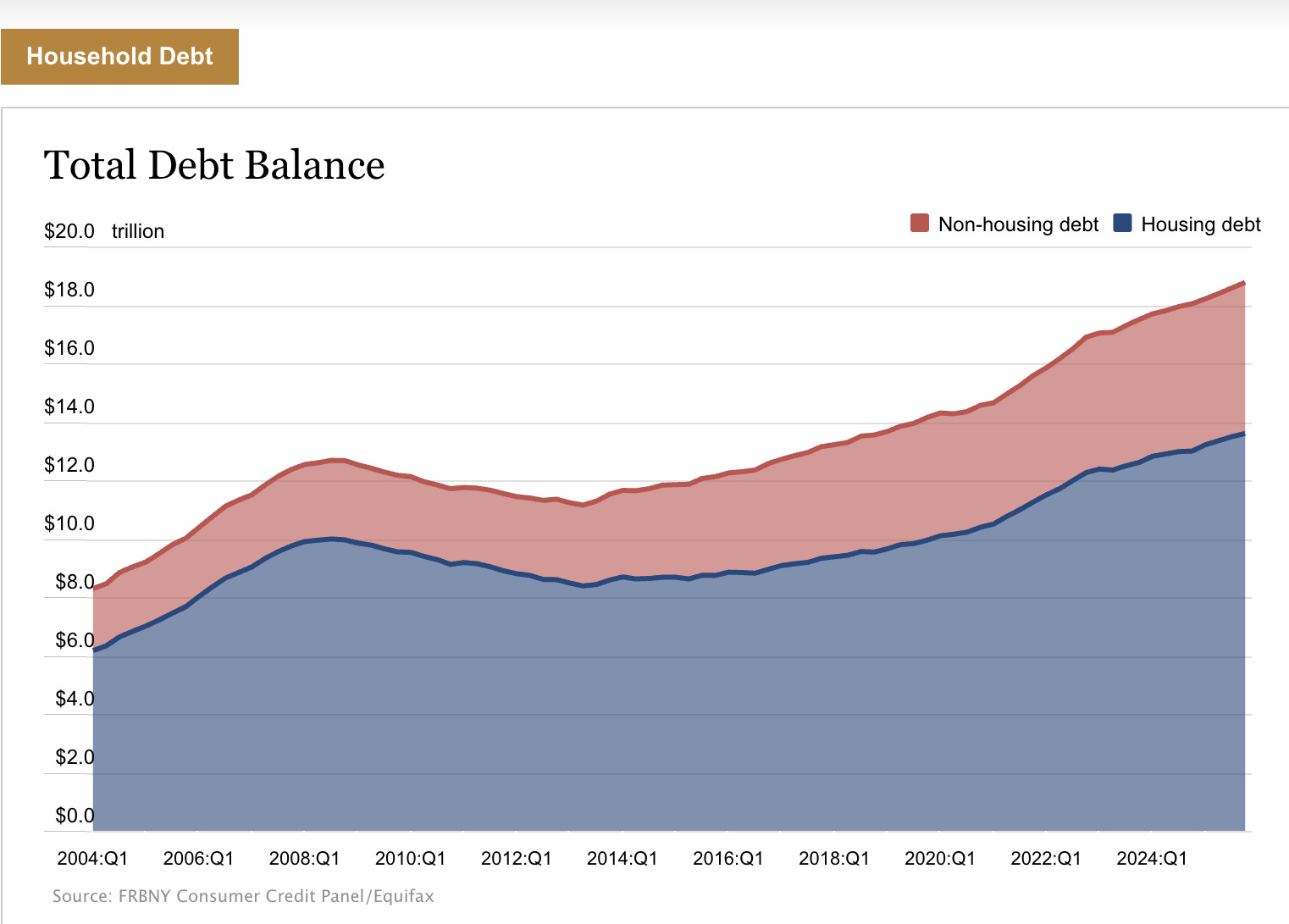

Debt across multiple categories

Credit cards are only one piece of the broader household debt picture.

The Household Debt and Credit Report from the Federal Reserve Bank of New York tracks several types of borrowing, including:

mortgages

auto loans

student loans

home equity lines of credit

Mortgage balances remain the largest category by far, reflecting the high cost of housing.

Auto loan balances have also grown in recent years as vehicle prices increased dramatically during supply chain disruptions.

Meanwhile, student loan payments resumed for many borrowers after pandemic-era pauses, adding another potential strain on household budgets.

Warning signs for consumer finances

Economists say the combination of high balances, rising interest rates, and growing delinquencies could create financial challenges if economic conditions weaken.

When households carry significant credit card debt, they often have less financial flexibility to deal with job losses, medical bills, or other unexpected expenses.

However, some analysts note that the overall financial system remains more stable than before the Great Recession.

Banks today generally maintain higher capital levels and more stringent lending standards, which reduces systemic risk even if consumer stress rises.

Still, for individual borrowers, the consequences of mounting credit card debt can be severe — including damaged credit scores, higher borrowing costs, and difficulty qualifying for loans.

A sign of the affordability squeeze

The growing reliance on credit to cover everyday costs reflects a broader economic challenge facing many households: the struggle to keep up with rising prices.

Even as inflation has moderated compared with its peak in 2022, many essential goods and services remain significantly more expensive than they were just a few years ago.

For millions of Americans, credit cards have become a financial cushion — but one that can quickly turn into a burden if balances continue to grow.

As policymakers monitor consumer finances, the data suggest that debt is increasingly playing a role not just in financing big purchases, but in helping households manage the day-to-day cost of living.

Great — here are three plug-and-play components you can drop directly into your story package: a sidebar, a data box, and SEO-friendly headlines.

Fraud Watch / Consumer Guide

5 warning signs your credit card debt is becoming dangerous

Credit cards can help consumers manage short-term expenses, but financial experts warn that balances can quickly spiral out of control when borrowing becomes routine rather than occasional.

Here are five warning signs that credit card debt may be becoming a serious financial problem.

1. You’re carrying a balance every month

If you rarely pay your full statement balance, interest charges begin accumulating immediately. With average credit card rates now above 20 percent, balances can grow quickly.

Financial counselors often advise treating credit cards like debit cards—charging only what you can pay off when the bill arrives.

2. Minimum payments barely reduce your balance

Many cardholders make only the minimum required payment each month. While this avoids late fees, it can take years—or even decades—to eliminate a balance because most of the payment goes toward interest rather than the principal.

For example, a $5,000 balance at 20 percent interest could take many years to pay off if only minimum payments are made.

3. You’re using credit for everyday essentials

Credit cards were traditionally used for major purchases or short-term borrowing.

But many households now report charging necessities such as groceries, utility bills, or rent. If routine expenses are being financed with credit, it may signal a deeper affordability problem.

4. Your balances keep increasing

Another warning sign is when balances continue to grow even though payments are being made.

This can happen when new charges exceed monthly payments or when high interest rates add significant costs.

5. You’re close to your credit limit

High credit utilization—using most of the available credit on a card—can damage credit scores and make lenders view borrowers as financially stressed.

Experts typically recommend keeping credit utilization below 30 percent of available credit.

Consumer tip:

If credit card debt becomes overwhelming, nonprofit credit counseling agencies may be able to help create repayment plans or negotiate lower interest rates.