Affordability Watch: Costs cool — but the squeeze isn’t over

Energy spikes return, food keeps climbing, and housing still weighs on budgets as new quarter begins

$6 gas in Southern California 4/1/2026. Staff photo

The post-inflation hangover

After a year of cooling inflation, the start of the quarter finds consumers in a familiar — and frustrating — position: prices aren’t surging like they were in 2022–2023, but they’re also not coming down.

Instead, the latest data show a shift. The inflation fight is no longer about runaway spikes. It’s about persistent, slow-burn increases across essentials — the kind that quietly erode household budgets month after month.

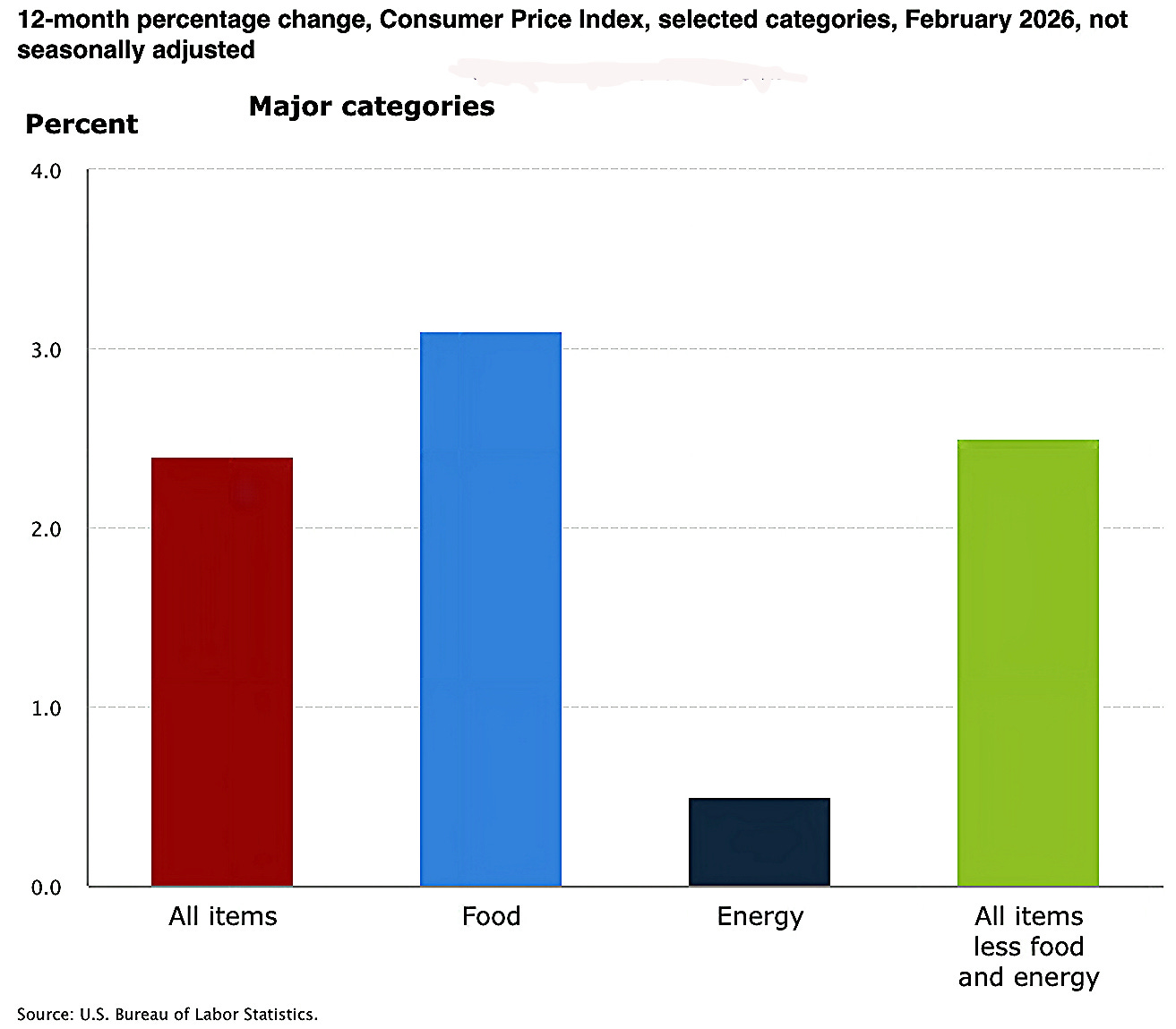

Headline inflation is now running around 2.4% annually, down from roughly 2.7% at the end of 2025. But that top-line number masks what consumers actually feel at the checkout line, the gas pump and the rent portal.

Energy: the comeback risk

The biggest change over the past three months is energy.

After declining late last year, energy costs are moving higher again:

Gasoline rose modestly in recent monthly data

Natural gas posted a sharp monthly jump

Electricity costs remain elevated year-over-year

More importantly, external pressures — including global supply concerns — are already pushing gas prices back toward $4 per gallon in some areas.

Why it matters:

Energy is the fastest-moving category in the economy. When it turns, everything else tends to follow — from shipping to groceries to utilities.

Affordability Watch takeaway: The brief window of energy relief may be closing.

Food: the quiet squeeze

Food inflation isn’t grabbing headlines — but it’s not letting up.

Recent data show:

Groceries rising about 0.4% per month

Dining out increasing at a similar pace

Restaurant inflation still running faster than grocery inflation annually

Over three months, that adds up to a noticeable increase — especially for households already stretched.

What’s driving it:

Labor costs in restaurants

Supply chain normalization (but not reversal)

Persistent pricing power in packaged goods

Affordability Watch takeaway: Food isn’t spiking — it’s compounding.

Housing: still the anchor cost

Housing remains the single biggest expense for most households — and it’s still rising.

The latest numbers show:

Shelter costs increasing modestly month-to-month

Rent growth slowing to its weakest pace in years

Annual housing inflation still around 3%

That slowdown is real — but it’s also limited.

The reality:

Even slower rent increases are building on top of already elevated prices from the past few years.

Affordability Watch takeaway: Housing pressure is easing — but not reversing.

Core essentials: the hidden pressure

Beyond food and energy, a range of everyday costs continue to rise steadily:

Medical care

Personal care products

Household goods and services

Core inflation sits around 2.5% annually, but many of these categories are running higher.

Why this matters:

These are the costs consumers can’t easily cut — and they’re becoming the new center of inflation pressure.

Affordability Watch takeaway: The squeeze is shifting from goods to services and necessities.

What this means

1. The inflation story has changed — but not ended

The crisis phase is over, but the affordability phase is not.

2. Relief is uneven

Goods: stabilizing

Services: still rising

Energy: volatile again

3. Consumers are stuck in a “high plateau”

Prices aren’t exploding — they’re staying elevated and inching higher.

4. Energy could reset the narrative quickly

A sustained rise in gas or utility costs could push inflation — and consumer stress — higher again.

Data box: Q4 affordability snapshot

Last ~3 months (Dec → Feb/March):

Energy: ⬆️ reversing upward

Food: ⬆️ steady monthly increases (~0.4%)

Housing: ⬆️ rising, but slowing

Core essentials: ⬆️ ~2.5% annually

Bottom line:

Prices are no longer surging — but they’re not falling

The burden is shifting to services, housing and energy

What to watch next

Gas prices heading into summer driving season

Grocery inflation persistence vs. wage growth

Rent trends as new supply hits the market

Credit card and auto loan delinquencies (the stress signal)