California advances bills to curb home insurance nonrenewals, force transparency on payouts

Measures would require clearer explanations for nonrenewals and give homeowners more time to fix issues and keep coverage

A legislative push to stabilize a shrinking insurance market

A set of California bills designed to protect homeowners from losing insurance coverage — and to ensure they receive the full benefits they paid for — has cleared a key hurdle in the state Senate.

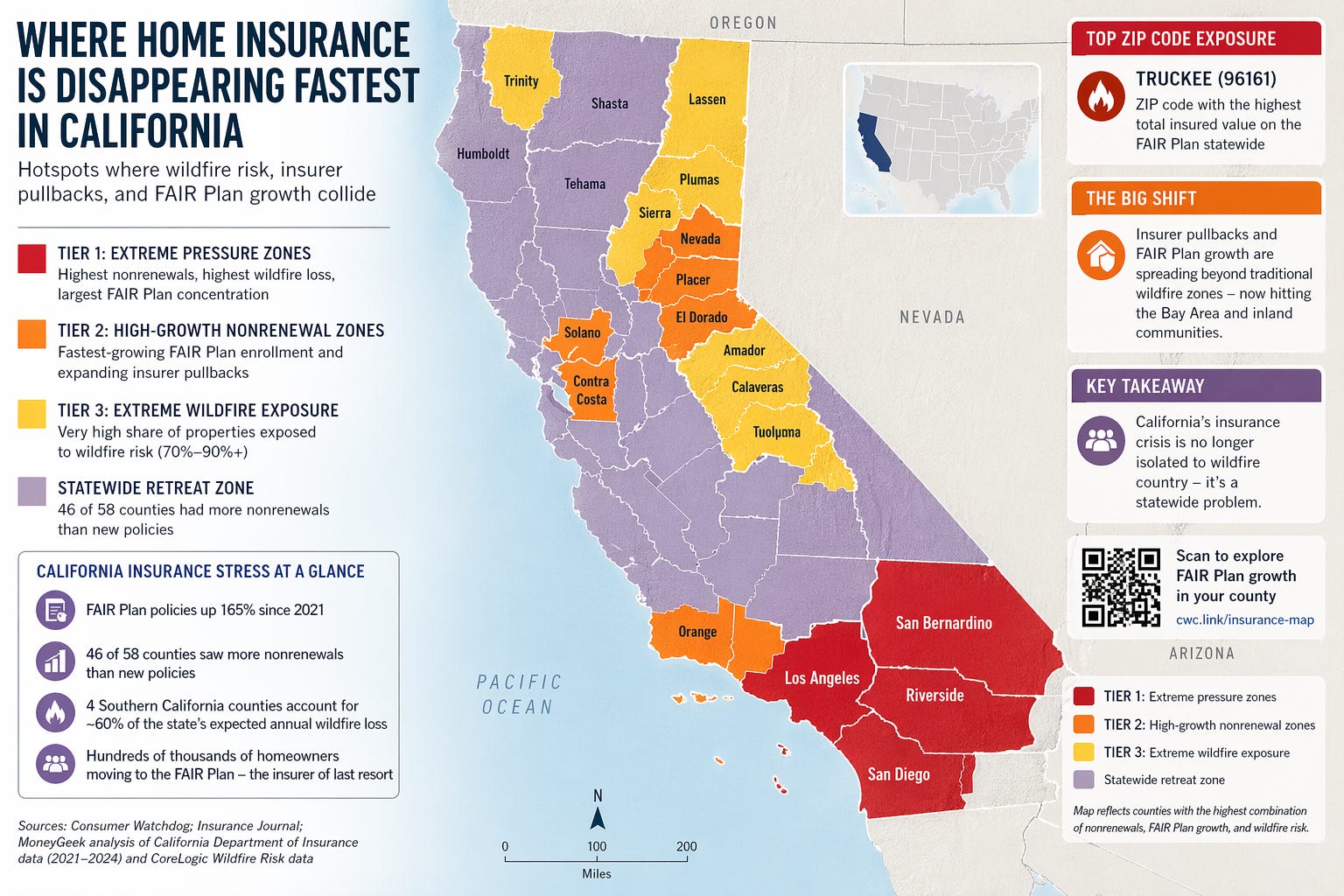

The package, backed by consumer advocates including Consumer Watchdog, passed the Senate Insurance Committee this week amid mounting concern over insurers pulling back from wildfire-prone areas and sharply raising premiums.

At the heart of the effort: stopping abrupt policy nonrenewals and forcing insurers to be more transparent about claims and coverage decisions.

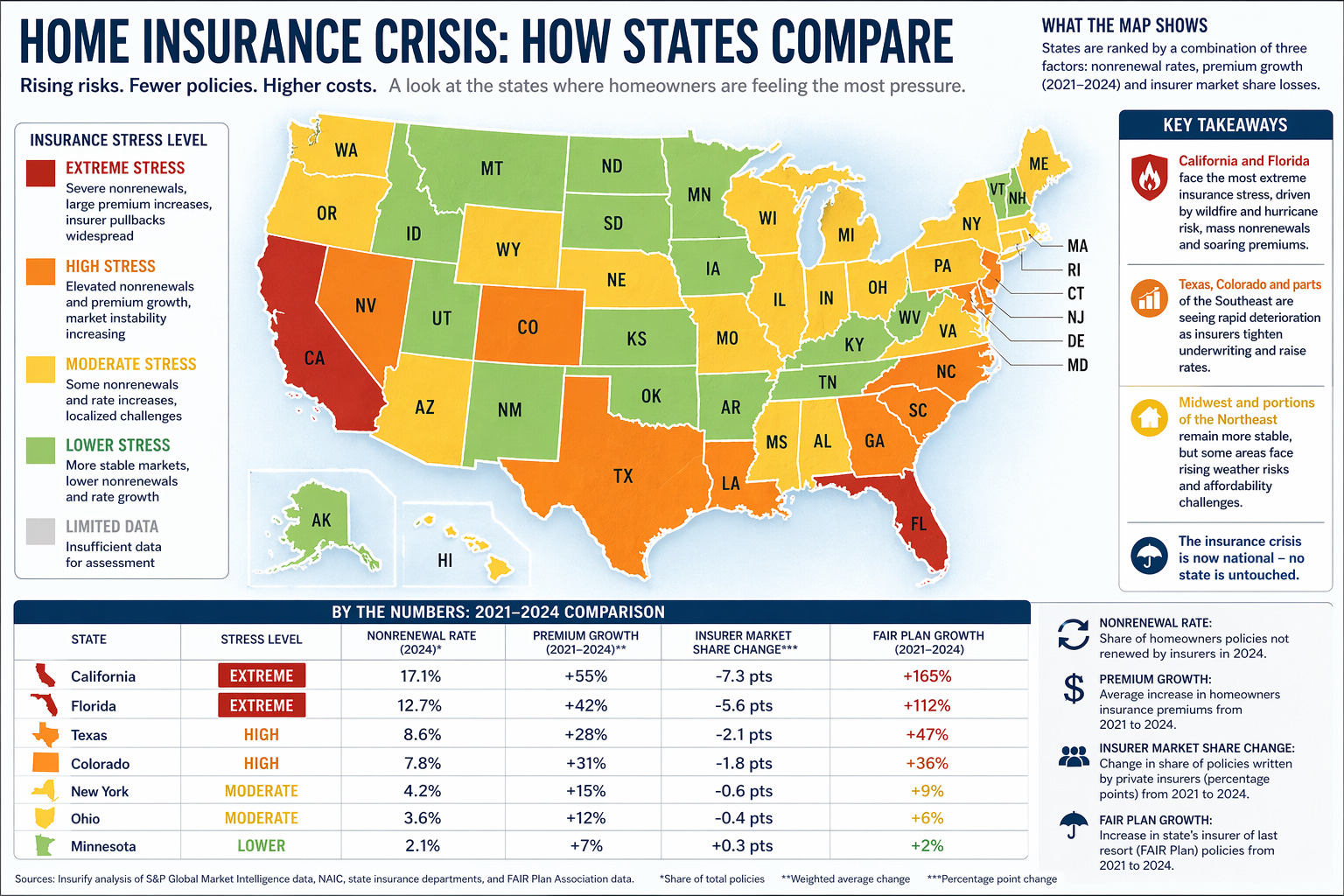

The measures come as California faces an ongoing insurance availability crisis tied to climate-driven wildfire risk and rising catastrophe losses, trends that have pushed insurers to limit exposure or exit markets altogether, according to the Yale Law Journal.

What the bills would do

The legislation targets several pain points for homeowners:

More time and transparency on nonrenewals

One bill would require insurers to give significantly more advance notice — up to six months — before refusing to renew a policy, along with detailed explanations of why the decision was made.

It would also give homeowners time to make repairs or correct errors in underwriting data to keep their coverage.

Guaranteed coverage for “fire-safe” homes

Another measure would require insurers to offer and renew policies for homes that meet state wildfire safety standards, such as defensible space and home hardening improvements, Insurance Journal reported.

Cracking down on claim underpayments and delays

Additional bills would force insurers to disclose how claim payouts are calculated — including original estimates and revisions — and impose penalties when payments are delayed.

Taken together, advocates say the package is meant to ensure homeowners can both keep their insurance and actually collect on it after a disaster.

Why this is happening now

The push reflects growing frustration among homeowners who say they are:

Being dropped despite making safety upgrades

Receiving little explanation for nonrenewal decisions

Struggling to recover full payouts after fires

Consumer groups argue that current rules give insurers too much discretion and too little accountability — especially as climate risks intensify.

Even existing protections, such as California’s one-year moratorium on nonrenewals after major disasters, have not prevented broader market pullbacks, the California Department of Insurance said.

Meanwhile, insurers contend that rising wildfire losses and rebuilding costs are forcing difficult underwriting decisions.

Industry concerns vs. consumer protections

The debate reflects a broader tension playing out across high-risk states:

Insurers warn that stricter rules could discourage companies from writing policies at all

Consumer advocates argue that without guardrails, coverage will continue to disappear — leaving homeowners stranded

According to reporting in Insurance Journal, the bills are part of a wider legislative push to balance insurer solvency with consumer access to coverage as the market destabilizes.

Data box: California insurance stress points

Nonrenewals rising in wildfire-prone regions

Climate change driving higher catastrophe losses globally

Insurance costs increasingly cited as a barrier to homeownership and rebuilding

Policyholders reporting disputes over claim payouts and delays

Sources: Consumer Watchdog; Insurance Journal; academic and policy research (

What this means for consumers

If enacted, the reforms could reshape how homeowners interact with insurers:

More time to respond: Longer notice periods could prevent sudden coverage gaps

Clearer rules: Required disclosures may make it easier to challenge nonrenewals

Potential leverage: Transparency in claims could help homeowners dispute low payouts

But the bigger question remains unresolved: whether stricter consumer protections will stabilize the market — or accelerate insurer pullbacks.

For now, California is emerging as a testing ground for how far states can go in regulating an insurance market increasingly shaped by climate risk.