CFPB rollback could weaken fair lending practices, consumer advocates say

Critics say the move could limit loans for mortgage, car loans, credit cards

A major shift in fair lending rules

A new rule issued this week by the Consumer Financial Protection Bureau is drawing sharp criticism from consumer advocates, who say it could significantly weaken protections against credit discrimination.

The rule alters how the agency enforces the Equal Credit Opportunity Act (ECOA), the nation’s primary law prohibiting discrimination in lending. Specifically, it removes or narrows the use of “disparate impact”—a legal doctrine that allows regulators to challenge practices that disproportionately harm protected groups, even without proof of intent.

The National Consumer Law Center (NCLC) called the move a “major step backward,” warning that it could expose borrowers to increased discrimination when seeking mortgages, auto loans, credit cards, or small-business financing.

What changed—and why it matters

Under the revised rule, regulators will have less authority to challenge lending practices that produce unequal outcomes across race, gender, or other protected categories unless intentional discrimination can be proven.

That’s a significant shift. Historically, disparate-impact analysis has been a cornerstone of civil rights enforcement in lending, housing, and employment.

Legal analysts say the CFPB’s changes also narrow other key provisions, including rules against discouraging applicants and guidance on special-purpose credit programs.

Supporters of the rollback argue that disparate-impact enforcement can be overly broad and create legal uncertainty for lenders. But critics say eliminating it removes one of the few tools capable of identifying systemic bias—especially in modern, algorithm-driven lending systems.

Who could be affected

Consumer advocates warn the impact could fall hardest on historically underserved groups, including:

Black and Latino borrowers

Native American communities

Older adults

Service members and veterans

These groups already face disparities in access to credit and loan pricing, and the new rule could exacerbate those gaps, according to the NCLC.

The concern is particularly acute as lenders increasingly rely on automated underwriting and artificial intelligence—tools that can replicate or amplify existing biases if left unchecked.

A broader pullback in consumer protections

The fair-lending rollback comes amid a wider shift in CFPB policy under the current administration.

Recent changes have included:

New hurdles for filing consumer complaints about credit reporting errors

Reduced regulatory scrutiny and enforcement activity

Efforts to limit how often consumers can submit complaints

Consumer advocates say these moves collectively make it harder for borrowers to challenge errors or unfair practices.

At the same time, complaint volumes have surged. The CFPB received more than 5.6 million complaints in 2025, with credit reporting issues accounting for the vast majority.

The policy and political backdrop

The rule aligns with a broader federal effort to scale back disparate-impact enforcement across agencies.

In recent days, the CFPB formally eliminated requirements tied to disparate-impact analysis under ECOA, a move critics say removes a key civil rights safeguard dating back decades, Reuters reported.

Advocates argue that without this framework, lenders could adopt policies that appear neutral but still disproportionately harm certain groups—without facing regulatory consequences.

Affordability Watch: Credit access meets rising costs

The timing of the rule change could amplify its real-world impact.

With borrowing costs elevated and household debt near record levels, access to fair and affordable credit is increasingly critical for consumers trying to:

Buy homes or vehicles

Start small businesses

Manage rising living expenses

Advocates warn that weakening fair-lending enforcement during an affordability crunch could lead to:

Higher loan denial rates for vulnerable borrowers

Wider gaps in interest rates and loan terms

Increased reliance on high-cost or predatory credit

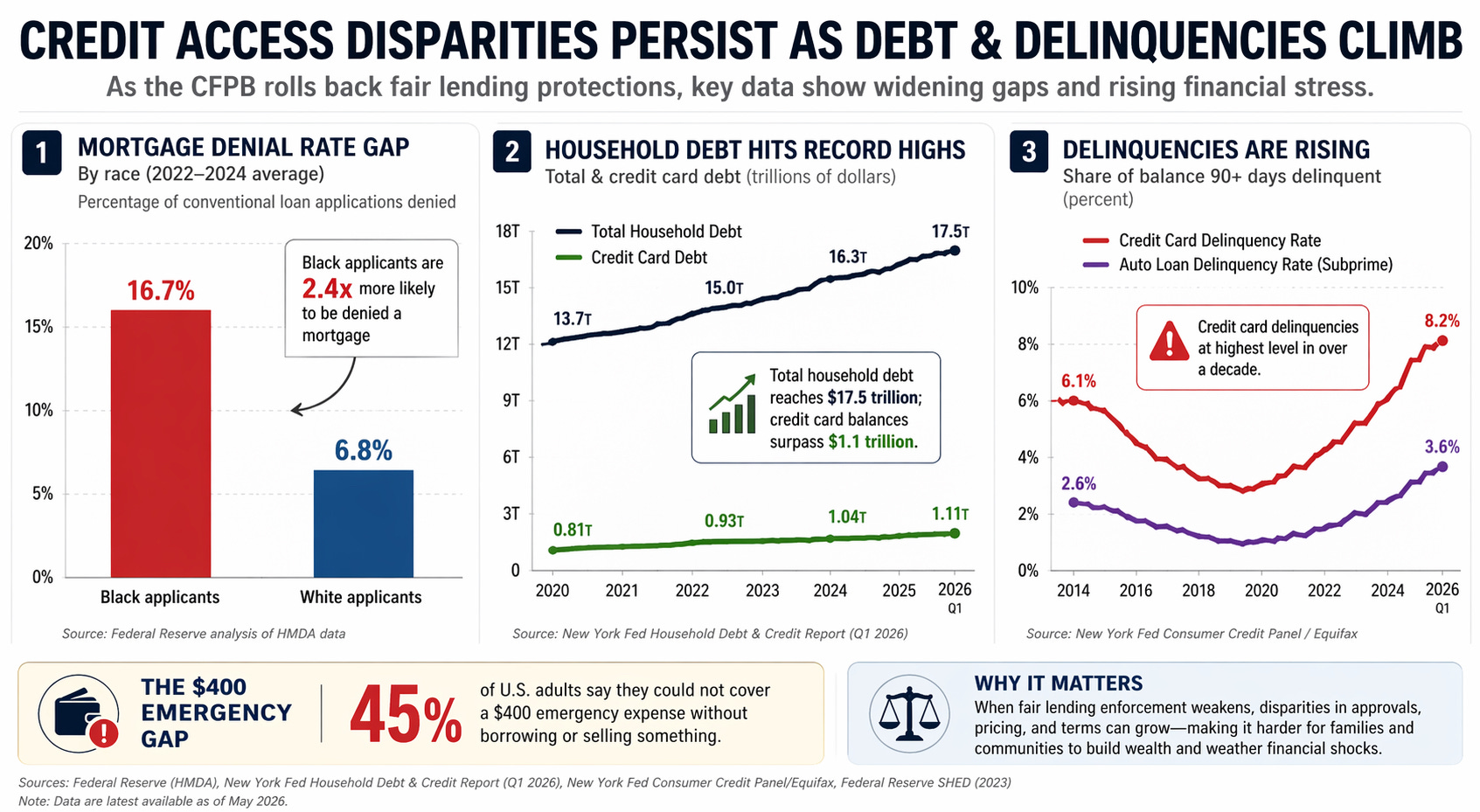

Data Box: Credit access and disparities by the numbers

Mortgage denial gaps persist

Black applicants: ~16–18% denial rate

White applicants: ~6–7% denial rate

(Federal Reserve HMDA data, recent years)

Higher borrowing costs for minority borrowers

Black and Latino borrowers are more likely to receive higher interest rates—even after controlling for income and credit score

(Consumer Financial Protection Bureau research findings)

Algorithmic bias concerns growing

Studies show fintech and AI-driven lenders can reduce some bias—but also risk replicating disparities embedded in historical data

(National Bureau of Economic Research working papers)

Household debt at record levels

Total U.S. household debt: ~$17.5 trillion

Credit card balances: over $1.1 trillion

(Federal Reserve Bank of New York Household Debt & Credit Report, 2025–2026)

Delinquencies rising in key categories

Credit card delinquency rates: highest in over a decade

Auto loan delinquencies: elevated, especially among subprime borrowers

(Federal Reserve Bank of New York)

Who relies most on credit access

~45% of U.S. adults say they could not cover a $400 emergency expense without borrowing or selling something

(Federal Reserve Survey of Household Economics & Decisionmaking)

Why this matters

When fair-lending enforcement weakens, these gaps can widen—affecting not just who gets approved, but how much they pay and what financial options remain available.

What comes next

Legal challenges to the rule are widely expected, and states or private litigants may attempt to fill enforcement gaps left by the CFPB.

But for now, consumer groups say the change represents a fundamental shift in how the federal government polices discrimination in lending—and one that could reshape access to credit across the U.S. economy.

What this means

For consumers, the changes are unlikely to show up as a single, obvious policy shift—but rather as subtle differences in who gets approved, at what price, and under what terms.

For regulators and lenders, the rollback signals a new era: one where proving discrimination may require showing intent—not just unequal outcomes—raising the bar for enforcement and potentially leaving more borrowers unprotected.