Condo fees surge nationwide, adding a new layer to the housing affordability crisis

Rising insurance, aging buildings and new safety rules are pushing monthly costs higher for millions of homeowners

The “fourth housing cost” is getting harder to ignore

For years, homebuyers focused on three core costs: mortgage, property taxes and insurance.

Now, a fourth expense is rapidly reshaping affordability — condo and homeowners association (HOA) fees.

Those monthly charges, once seen as relatively modest, are rising sharply across the country, adding hundreds — and sometimes thousands — of dollars to the cost of owning a home.

Recent data from Realtor.com shows condo fees have climbed to a median of about $420 per month in 2025, up roughly 29% since 2019. Even single-family homes with HOAs are seeing similar increases.

And the reach of those fees is expanding. About 43.6% of listings now include HOA dues, up from 34.3% just a few years ago — meaning buyers increasingly can’t sidestep them.

What homeowners are paying now

While national averages can look manageable at first glance, the reality for condo owners is far more expensive.

Typical condo fees now run:

$400 to $500 per month nationwide

$1,000 or more in high-cost markets

In places like New York City, more than half of condo owners pay at least $500 monthly — and many pay far more.

Altogether, roughly 22 million U.S. households are now paying HOA or condo fees, turning what was once a niche expense into a major line item in household budgets.

Why fees are rising so quickly

The surge isn’t driven by a single factor — it’s the result of several overlapping pressures that are unlikely to ease anytime soon.

Insurance costs are exploding

The biggest driver is insurance.

HOAs insure entire buildings, not just individual units. As property insurance premiums rise — especially in disaster-prone states — those costs are passed directly to homeowners.

In states like Florida and California, insurers have pulled back or raised rates dramatically, leaving associations scrambling to cover higher premiums.

New safety laws are forcing higher reserves

The 2021 condo collapse in Surfside, Florida triggered sweeping regulatory changes.

States — particularly Florida — now require:

More frequent structural inspections

Fully funded repair reserves

Some California cities, including Los Angeles, have required upgrading of older foundations to make them more earthquake-resistant.

That means HOAs can no longer delay costly repairs or underfund long-term maintenance — a practice that kept fees artificially low for years.

Now, many associations are raising dues sharply or issuing special assessments to catch up.

Aging buildings need expensive repairs

A large share of U.S. condo buildings were built decades ago and are entering a costly phase of their lifecycle.

Major expenses include:

Roof replacements

Structural repairs

Elevator upgrades

Plumbing and electrical systems

Many associations had deferred these costs — and are now facing large bills all at once.

Inflation is hitting every line item

Routine expenses have also risen:

Labor costs for maintenance workers

Materials for repairs

Utilities and landscaping

Even well-managed buildings are seeing steady fee increases just to keep up.

Amenities are raising the baseline

Modern developments increasingly offer:

Gyms and pools

Security and concierge services

Shared workspaces

Those amenities come with ongoing operating costs — locking in higher monthly fees.

Florida is the epicenter — but isn’t alone

Fee increases are happening nationwide, but Florida stands out.

Cities like Miami and Naples now report median HOA fees well above $600 per month, among the highest in the country.

The reasons are clear:

A heavy concentration of condo buildings

Surging insurance costs tied to hurricane risk

New safety regulations

But other high-cost markets — including New York, Hawaii and parts of California — are seeing similar pressures.

Affordability Watch: when “cheaper” homes aren’t cheaper anymore

Condos have long been marketed as an affordable entry point into homeownership.

That assumption is breaking down.

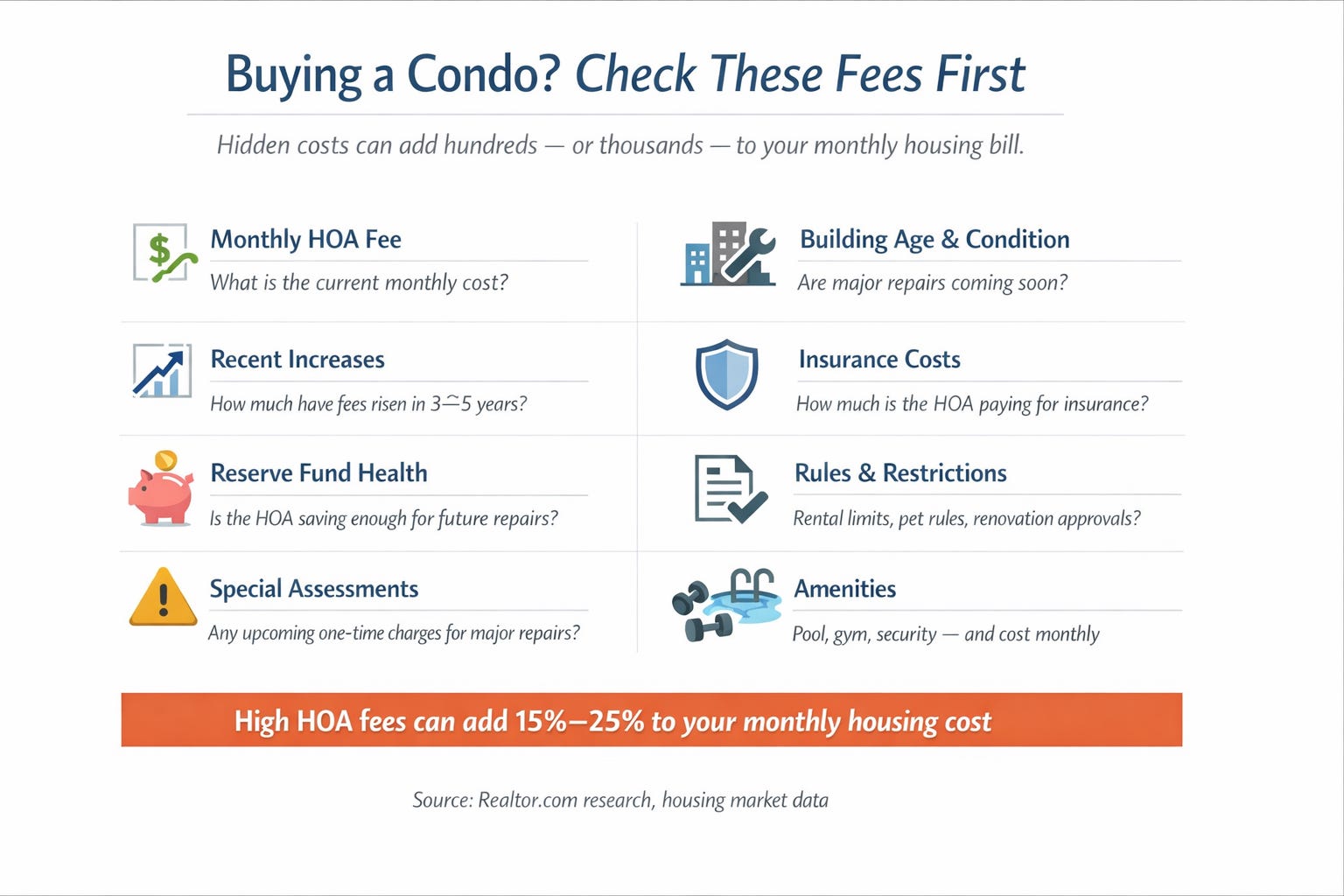

In some markets, HOA fees now account for 15% to 25% of a monthly housing payment, significantly eroding the savings from a lower purchase price.

For buyers, that creates a new reality:

A lower-priced condo may carry higher total monthly costs than a more expensive single-family home without fees

Rising dues can push owners into financial strain even after purchase

Economists say the shift is changing how buyers evaluate homes — with monthly cost, not purchase price, becoming the key metric.

What this means

The rise in condo and HOA fees is more than a nuisance — it’s a structural shift in housing costs.

For buyers:

Monthly affordability calculations must include HOA fees upfront

Future increases are likely, not optional

For current owners:

Rising dues may strain budgets

Special assessments could add unexpected costs

For the housing market:

Condos may lose their traditional role as “starter homes”

High fees could weigh on resale values in some markets

Data box

$420/month — Median condo fee (2025)

+29% — Increase since 2019

43.6% — Share of listings with HOA fees

~22 million — U.S. households paying HOA dues

$1,000+ — Common monthly fee in high-cost markets

The bottom line

Condo and HOA fees are no longer a footnote in the cost of homeownership.

They are increasingly a core driver of affordability — and a growing source of financial pressure for millions of Americans.

As insurance costs rise, buildings age and regulations tighten, those fees are likely to keep climbing — reshaping the economics of homeownership in the process.

The author is an HOA board member in Los Angeles.