Credit-card debt hits $1.25 trillion as families slip into ‘survival debt’

Brands shrinking sizes, expanding value packs to hang onto customers

Total U.S. credit-card debt has reached $1.25 trillion, and delinquencies are climbing toward the highest level since the financial crisis, according to The Wall Street Journal.

The Journal profiled Catherine Clarke, 42, who earns $194,000 a year but watched a Chase Sapphire balance grow to $15,000 at a 26 percent annual interest rate, with a $572 monthly minimum that barely dented the principal, the Journal reported.

The story has resonated because it is no longer a problem confined to the lowest income brackets. Even with a high salary, “soaring interest rates and stubborn inflation have led to the highest delinquencies since the financial crisis,” the Journal reported, with more families shifting into “a pattern of survival debt.”

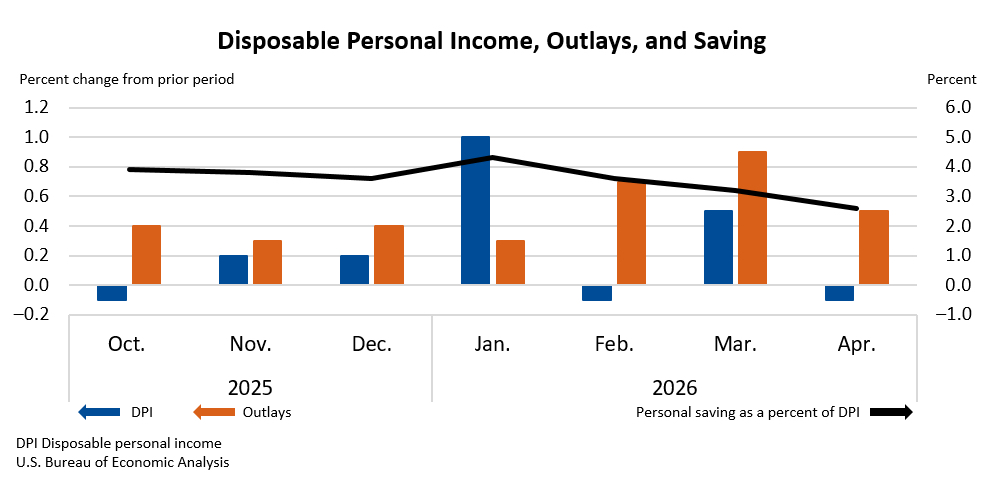

That pattern fits the broader picture coming out of Thursday’s BEA release: spending up but flat after adjusting for inflation, incomes stagnant, savings rate near record lows, and a growing share of households turning to revolving credit to cover groceries, gasoline and electric bills.

Big brands take action to hang onto customers

The corporate response is starting to shift. The Wall Street Journal reported Thursday that companies including Clorox and Kraft Heinz are conceding that significant portions of their customer base can no longer afford their products at current prices, and are beginning to cut prices or expand value packs.

Dollar Tree Chief Executive Michael Creedon Jr. said on the company’s earnings call that “lower-income” customers are “navigating higher fuel costs and broader macro uncertainty” and are “shopping more thoughtfully and closer to their immediate needs,” The New York Times reported.

The playbook keeps tightening

To put it simply, the consumer is running out of slack. April’s economic reports showed that inflation is still beating wages and that families are dipping into savings simply to stay even.

The Iran negotiations could give the Fed and the household budget a reprieve, but the truce is tentative, gasoline is still up nearly 50 percent since the conflict began, and the strait’s tolling fight is unresolved.

Costco’s quarter shows what is working in this economy — bulk buying and discount fuel — and reveals what is breaking elsewhere, with lower-income shoppers boxed in. Housing remains stalled at 6.5-plus percent mortgages, draining the wealth-building channel most middle-class families relied on. And the $1.25 trillion credit-card balance is the bill for all of it: when paychecks cannot stretch, the plastic does.

For consumers, the practical playbook tightens with each Friday report: lock in fixed-rate borrowing if it is still available, treat savings goals as a fixed expense rather than a residual, and watch the next jobs report and gas-price reading like a hawk.

For policymakers, the message Kevin Warsh inherits is unambiguous. With inflation at 3.8 percent, incomes flat, and a foreign-policy crisis still capable of moving the pump price overnight, the path back to a 2 percent target — and to the rate cuts most households are counting on — has rarely looked longer.