Inflation hit a three-year high in May, and energy did almost all of it

No relief in sight as Middle East troubles drag on

The Labor Department reported Wednesday morning that the Consumer Price Index rose 0.5 percent in May and 4.2 percent over the past year, up from 3.8 percent in April and the hottest annual figure since April 2023.

Energy did almost all the work. Energy prices rose 3.9 percent on the month and 23.5 percent over the past year, CNBC reported, and the Labor Department said energy accounted for more than 60 percent of the monthly CPI increase.

Gasoline alone jumped 40.5 percent from a year earlier. Airline fares climbed 2.7 percent on the month as carriers passed energy costs through. Shelter rose a more modest 0.3 percent and is up 3.4 percent annually.

Used cars ticked up 0.1 percent, new vehicles fell 0.3 percent, and motor-vehicle insurance dropped 1.7 percent — a rare bright spot in a report dominated by what gets pumped into a tank.

Eating gets expensive

Groceries kept squeezing households. Food at home rose 2.7 percent from a year earlier and overall food prices ticked up 0.2 percent on the month, CNBC reported.

“Inflation is painfully high,” Mark Zandi, chief economist at Moody’s, told CNBC; he said the rate is likely near a peak but will not return to anything that feels reassuring to consumers for roughly a year.

Heather Long, chief economist at Navy Federal Credit Union, told CNBC that gasoline, groceries, electricity and health care are all running above 3 percent annually — the categories Americans encounter every week.

The market reaction was unambiguous. The Dow Jones Industrial Average closed down 953 points, a 1.9 percent loss, The Wall Street Journal reported; the Nasdaq composite fell 2 percent and the S&P 500 lost about 1.6 percent, with industrial stocks the hardest hit and eight of 11 S&P sectors lower on the day.

President Trump greeted the print with a Truth Social post saying “I love the inflation,” tying his remark to plans for new tariffs. The Wall Street Journal’s analysis of paycheck math was less rosy: “Wage Gains Wiped Out by Gas Prices,” its CPI live blog summarized.

Oil climbs back above $92

Wednesday’s market drop happened against a louder geopolitical backdrop. U.S. forces launched a second day of strikes against Iran, and Tehran “fires back and says” it will not relent, NBC News reported in a live blog. President Trump “pledges Tehran will ‘pay the price’ for not accepting deal,” CBS News reported on its live updates page, after Iran shot down an Army Apache helicopter near the Strait of Hormuz Monday.

Energy markets did not need to be told twice. WTI crude futures climbed 2.9 percent in early Asian trading Thursday to roughly $92 a barrel as supply-disruption fears returned. Rystad Energy warned that “if hostilities resume in earnest” prices could “move towards $150 per barrel,” The Wall Street Journal reported.

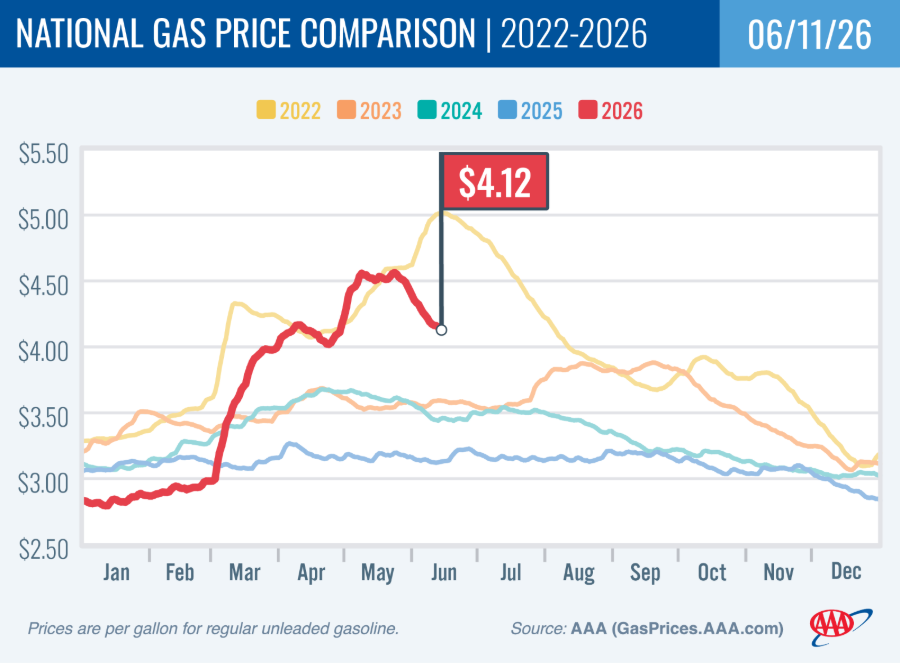

At the pump, the squeeze is already on. The Energy Information Administration’s June 1 reading had retail gasoline at $4.31 a gallon, up 38 percent from $3.13 a year earlier and from $4.12 on April 27. Prices have eased slightly to about $4.15-$4.16 in AAA and EIA data since, the Associated Press reported, and a gallon has now been above $4 every day since March.

“The Middle East situation is still unresolved,” Bjornar Tonhaugen of Rystad told CNBC, warning that if the strait stays closed, oil could escalate to $140 a barrel or more by October or November. Zandi added that even if the conflict de-escalates, oil and gasoline prices are likely to remain above pre-war levels because traders will price in future Hormuz risk indefinitely.

The New York Times’ interactive gas-price map, updated this week, showed the West Coast and Northeast bearing the brunt of the increase.