No state meets basic protections for debt-burdened families, report finds

States fail to offer effective help to working poor families

• New report finds no state meets basic protections for debt-burdened families

• Six states earn ‘B’ grades; nine receive failing marks

• Real debtors’ stories highlight dangers of weak exemption laws

No U.S. state currently provides all the core legal protections families need to shield income and essential property from seizure by creditors, according to No Fresh Start, a new national analysis by the National Consumer Law Center (NCLC). The annual report evaluates state “exemption laws,” which are meant to prevent creditors, debt buyers, and debt collectors from taking income and assets that families need to survive and work.

“These protections are critically important today,” the report states, as families cope with historically high inflation, rising costs of rent and food, and a surge in debt collection lawsuits.

Why exemptions matter

Exemption laws determine how much of a consumer’s wages or property can be seized after a creditor obtains a court judgment. If protections are weak, creditors can drain wages, seize cars, lien and even force sale of homes.

The report opens with a vivid example: Stacey Knoll, a mother of three in Colorado, who watched her paycheck garnished to pay an $881 medical bill that had swelled with interest and fees. “And that’s when I got that garnishment from the court,” Knoll said. “It was really scary. I’d never been on my own or raised kids on my own.”

The report emphasizes that exemption laws are key to keeping families out of poverty and enabling them to “be productive members of society and regain financial stability.”

Five standards no state meets

Despite their importance, no state meets all five basic standards identified by the report:

Preventing creditors from garnishing so much of a debtor’s wages that the worker is pushed below a living wage;

Allowing a debtor to keep a used car of at least close to average value;

Preserving the family’s home at least up to median value;

Preserving a basic amount in a bank account for essential costs including rent and utilities;

Preventing seizure and sale of necessary household goods.

“These standards represent a basic floor for economic stability,” the authors write.

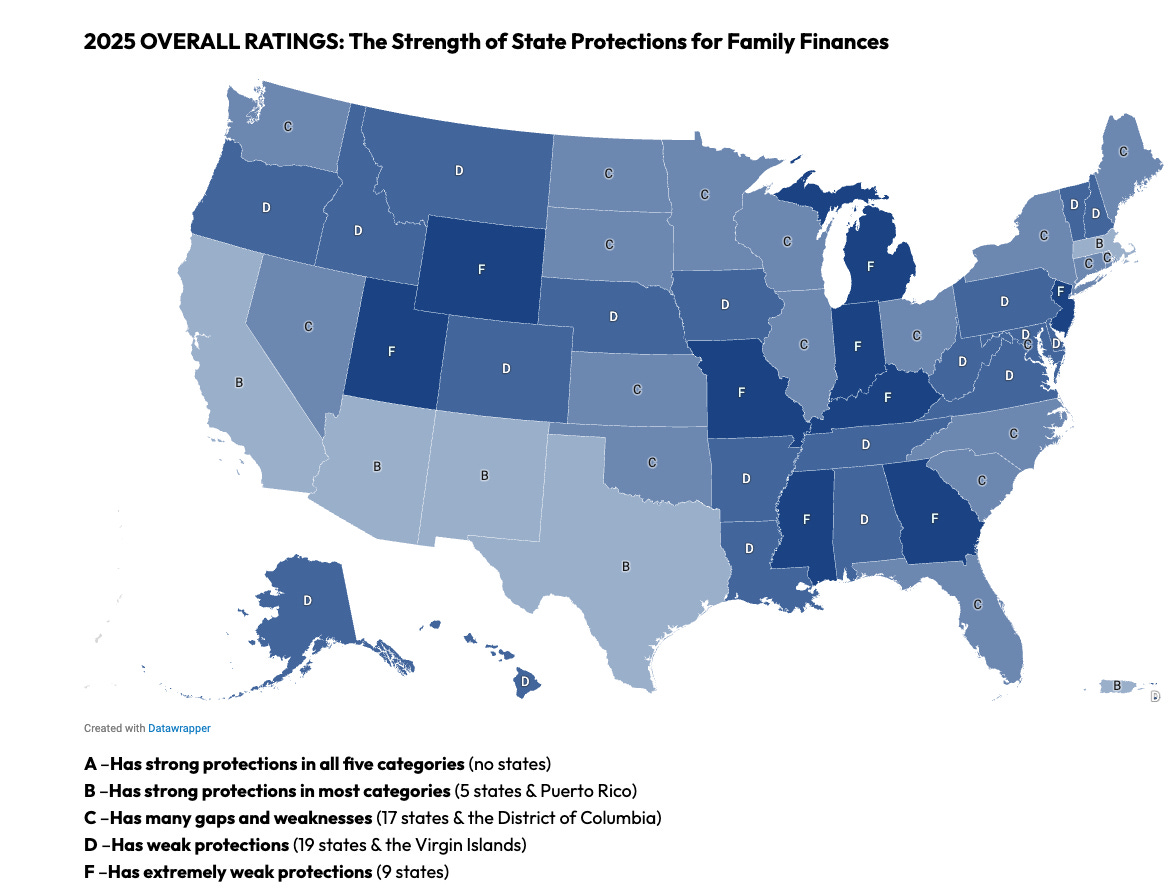

Best performers still fall short

Although no state earned an ‘A’ grade, six jurisdictions received ‘B’ grades for 2025: Arizona, California, Massachusetts, New Mexico, Puerto Rico, and Texas. These states offer comparatively stronger protections but still fail to fully safeguard families.

“These states are closer to providing meaningful protection,” the report notes, but “even they fail to meet all of the core standards families need.”

Worst states allow broad seizure

At the opposite end of the scale are states with long-standing weak protections, earning ‘F’ grades for 2025: Georgia, Indiana, Kentucky, Michigan, Mississippi, Missouri, New Jersey, Utah, and Wyoming. The report says these states’ laws “reflect indifference to struggling debtors” by allowing seizure of nearly all assets—even the minimal items necessary to continue working and supporting a family.

Michigan nearly improved its standing after both legislative chambers passed a bill in 2024 that would have strengthened exemption protections. However, the House failed to send the measure to the governor for signature, and the question is now before the state supreme court.

Calls for reform

The authors argue that stronger, self-executing exemption protections — where courts automatically shield exempt income and assets without additional legal filings — could help prevent families from falling deeper into hardship after a debt judgment.

Without such reforms, advocates warn, “exemption laws … drain away the wages and resources that families need—and that the local economy needs them to be spending at Main Street businesses.”

Absolutely — here are state-by-state highlights based on the 2025 No Fresh Start report, showing how individual states stack up on key protections under their exemption laws. These focus on wage protection, bank accounts, cars, homes, and whether protections are self-executing — all factors that determine how well families can stay afloat financially after a debt judgment.

State-by-State Highlights: How Well Protections Hold Up

Best Overall ( ‘B’ Grade States )

These states have stronger laws than most, but still do not satisfy all core protections:

Arizona – Protects a relatively large share of wages and allows a decent homestead exemption; includes automatic inflation adjustments for some exemptions.

California – Offers comparatively robust protections for homes and some wages, and recently enacted stronger consumer finance laws more broadly (e.g., preventing medical debt from harming credit scores). (Governor of California)

Massachusetts – Provides solid exemptions across multiple categories, though gaps remain.

New Mexico – Offers stronger property protections compared with most states.

Puerto Rico – On par with the best U.S. states in shielding assets and income.

Texas – Known for high homestead and other exemptions relative to many states, though still not meeting all standards.

Takeaway: These states tend to protect wages, cars, and some bank assets better than average — though none fully prevents seizures that could jeopardize a family’s economic stability.

Worst Overall ( ‘F’ Grade States )

These states consistently fail to preserve basic financial protections:

Georgia – Permits very limited wage or asset protection, exposing families to deep hardship.

Indiana – Weak homestead and wage protections leave many families vulnerable to garnishment.

Kentucky – Offers minimal exemptions that do little to safeguard living wages or essential property.

Michigan – Came close to improving protections with 2024 legislation, but reforms stalled in the legislature and are now before the state supreme court.

Mississippi – Provides a low homestead exemption with only a small “wildcard” that’s rarely enough to protect essentials.

Missouri – Weak protections across multiple categories.

New Jersey – Limited wage and asset safeguards leave residents exposed.

Utah – Exemptions often fail to cover a median-value car or home.

Wyoming – Lacks meaningful protections for wage earners and essential property.

Takeaway: In these states, creditors or collectors can seize nearly all a debtor owns — including wages and items needed to support work and family life.

Other Notable Patterns Across States

Wage Seizure Protections

Some states go beyond federal minimums to protect a worker’s paycheck. Still, only about 14 jurisdictions protect even a poverty-level wage for a family of four, and several do not exceed federal minimum protections at all.

Highlights: States like California and Arizona tend to offer stronger wage protection than many others.

Cars and Transportation

Exempting a car of near-average value is crucial — losing a vehicle often means losing employment.

Some states offer higher value exemptions or “wildcard” exemptions that debtors can apply to transportation. Others have outdated low caps that do little to keep workers mobile.

Homestead/Home Protections

Homestead exemptions vary widely: some states protect median-value homes, while others offer tiny caps that do little in high-housing-cost areas.

Bank Account Protections

States differ in whether exemptions are self-executing (automatically applied), which greatly affects whether debtors actually benefit without going back to court.

Household Goods

Many states still allow seizure and sale of essential household items, leaving families without basic furnishings and appliances.

What This Means for Families

The No Fresh Start report shows that weak exemption laws can strip families of wages, cars, homes, and bank funds — pushing them deeper into poverty after falling behind on debt.

Advocates say states should strengthen laws with self-executing protections, higher exemption caps, and clearer safeguards for wages and essential property to help families regain stability.