Security deposit ‘alternatives’ may leave renters paying more — with fewer protections

A new report warns that security deposit “alternative” products can cost tenants more than traditional deposits while stripping away key legal protections

A new consumer advocacy report is warning that a rapidly growing class of rental housing financial products may be worsening the affordability crisis for millions of tenants.

The report, released today by the National Consumer Law Center, argues that so-called security deposit “alternatives” frequently leave renters paying more money overall while weakening legal protections that traditionally apply to security deposits.

The products are increasingly marketed by “PropTech” — or property technology — firms and landlords as a substitute for traditional security deposits. Instead of paying a refundable lump-sum deposit upfront, tenants pay recurring fees or purchase insurance-like products that allow them to move into an apartment with lower initial cash costs.

But according to the NCLC report, many renters ultimately pay far more than they would under a standard deposit arrangement because the fees are generally nonrefundable and continue month after month.

“Security deposit alternative products attempt to evade state laws designed to protect tenants,” said April Kuehnhoff, a senior attorney at NCLC and co-author of the report.

Additional financial risks

The report also alleges that some products expose renters to additional financial risks, including debt collection actions tied to landlord damage claims. In some cases, the companies may seek reimbursement directly from tenants after paying landlords, effectively functioning more like a loan obligation than a traditional deposit.

“People pay and pay, but at the end of the lease none of the fees are refunded, unlike a traditional security deposit,” said Steve Sharpe, another senior attorney at NCLC. “On top of that, they can face debt collection to reimburse the PropTech company.”

Housing affordability pressures have made the products increasingly attractive to renters struggling to cover steep move-in costs. In many cities, tenants must come up with first month’s rent, last month’s rent, application fees, broker fees and security deposits all at once — often totaling thousands of dollars.

Consumer advocates say that financial pressure has opened the door for new fee-based products marketed as affordability solutions.

Data Box: Why this matters

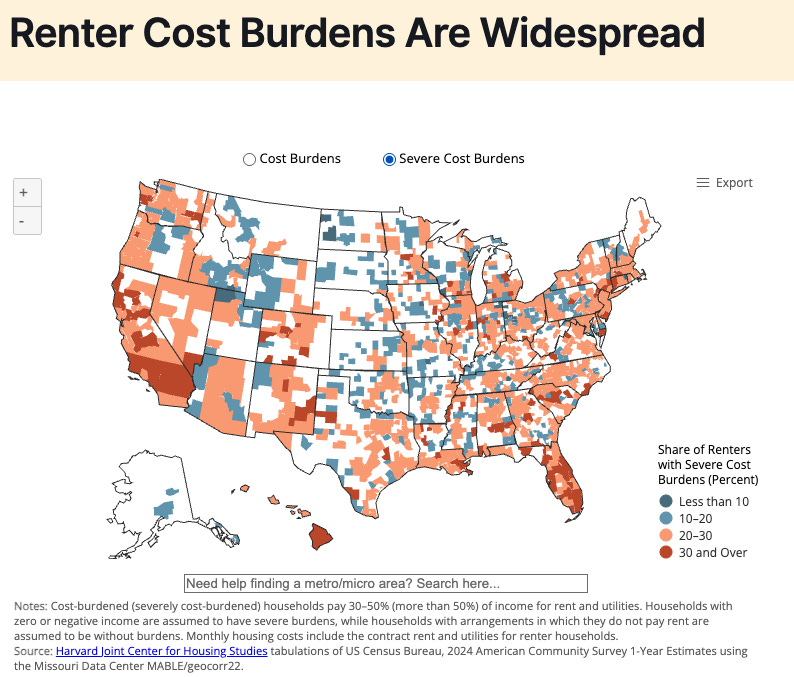

More than half of Black renters and Hispanic renters are considered cost burdened, according to Harvard housing researchers.

Security deposit alternatives often involve monthly nonrefundable fees instead of refundable deposits.

Consumer groups say renters can still face debt collection even after paying the recurring fees.

PropTech firms are becoming increasingly involved in rent collection, screening and lease management nationwide.

Renters facing heavier burdens

The issue comes as renters nationwide continue to face heavy financial burdens. Data from Harvard Joint Center for Housing Studies cited in the report found that more than half of Black renters and Hispanic renters are considered “cost burdened,” meaning they spend more than 30% of their income on housing and utilities.

The report also connects the issue to broader concerns about algorithmic tenant screening and “junk fees” in the rental market. Consumer advocates have increasingly criticized landlords and PropTech firms for layering on technology-driven charges that can include application fees, mandatory “convenience” charges, lease processing fees and tenant screening costs.

Federal regulators have also been scrutinizing rental junk fees more aggressively in recent years. The Federal Trade Commission has proposed broader crackdowns on hidden or misleading fees across multiple industries, while the Consumer Financial Protection Bureau previously warned about abusive practices tied to tenant screening and rental payment systems.

Housing advocates say traditional security deposits, while often expensive upfront, are at least subject to longstanding state laws governing how the money must be held, when it must be returned and what deductions landlords may legally make.

By contrast, many deposit “alternative” products operate in legal gray areas because they are structured as fees, insurance products or guarantees rather than deposits.

The NCLC report urges state and local governments to strengthen tenant protections, regulate rental junk fees and expand access to safer alternatives for renters struggling with move-in costs.

“Local governments can increase access to traditional security deposits, increase enforcement of existing laws, and prohibit abusive practices,” said Ariel Nelson.

What renters should watch for

Consumer advocates recommend tenants carefully review any security deposit “alternative” product before signing a lease. Key questions include:

Are the fees refundable?

Is the tenant still liable for damages after paying fees?

Can the company send unpaid claims to collections?

Does the landlord still have access to traditional eviction or damage claims?

Are automatic bank withdrawals authorized in the contract?

Advocates also suggest comparing the total long-term cost of recurring fees against a one-time refundable security deposit.