Surprise! Your health insurance just got way more expensive

Millions of Americans discover the enhanced ACA subsidies they’d been counting on have quietly vanished

In news that will shock absolutely no one who’s been paying attention to Congress, enhanced Affordable Care Act subsidies expired Thursday, immediately driving up monthly premiums for more than 20 million Americans who were apparently supposed to just know this was coming.

“I thought it was a mistake,” one self-employed Ohio policyholder told reporters after her monthly premium skyrocketed from $120 to over $400. Spoiler alert: it wasn’t a mistake. It was democracy in action.

The subsidies, which were first expanded in 2021 as a pandemic-era lifeline and extended through 2025, made health insurance actually affordable for middle-income families, early retirees, gig workers, and small business owners. Naturally, Congress let them expire.

What Just Happened?

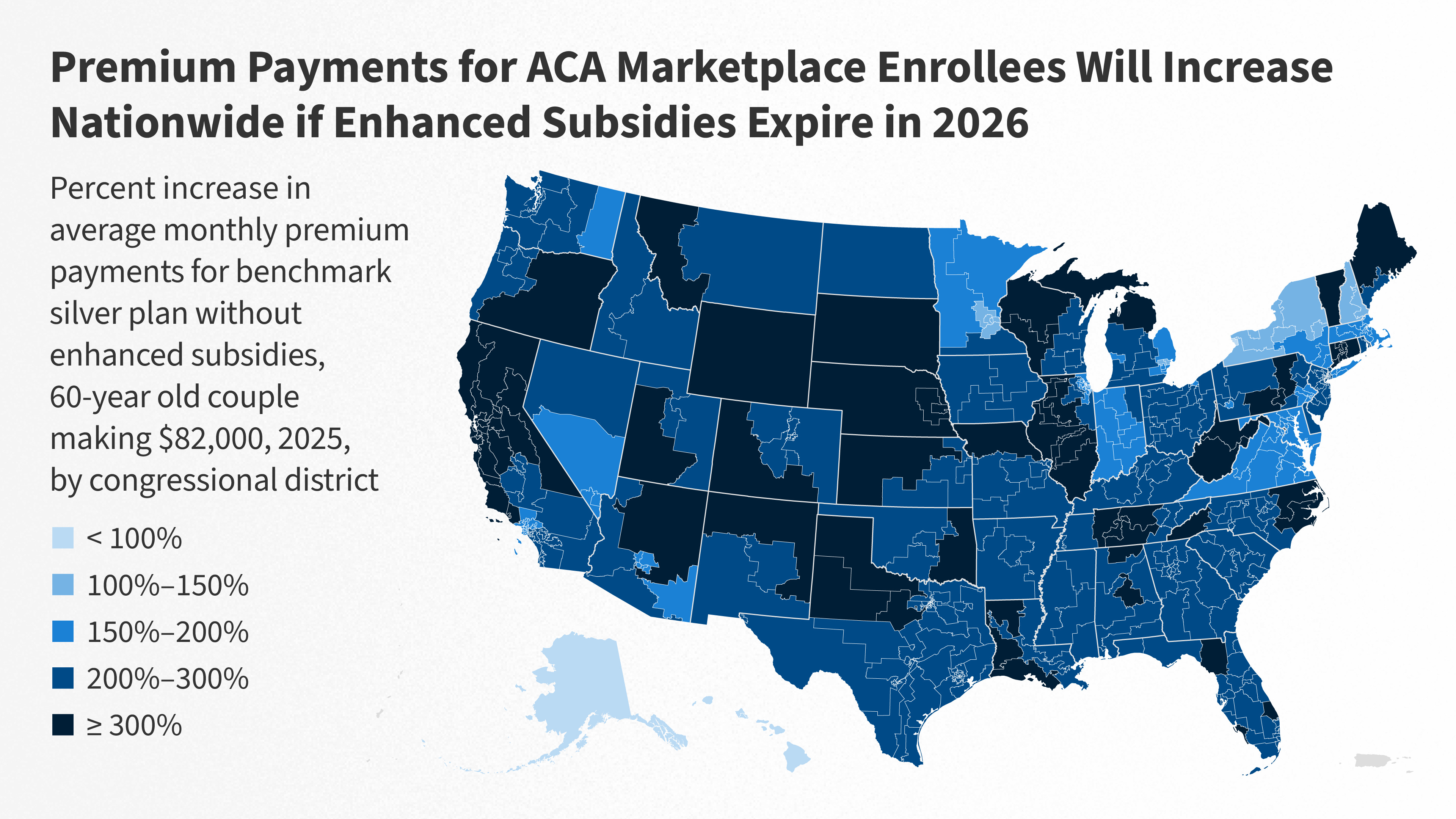

The enhanced subsidies had eliminated the so-called “subsidy cliff” — that fun feature of the original ACA where earning just slightly too much money meant you suddenly qualified for zero help. They also increased tax credits across the board, making coverage genuinely affordable for millions who’d never qualified before.

Now those enhancements are gone, and the original ACA rules have snapped back into place like a rubber band aimed at your wallet. Many enrollees will receive smaller tax credits, some higher-income households will get nothing at all, and net premiums are rising even when insurers’ base rates stay flat.

Policy analysts estimate millions of enrollees now face premium increases of 25% to 100% or more, depending on income, age, and location. But hey, at least they can still technically afford to think about health insurance.

Nobody Warned Us (Except Everyone Who Was Paying Attention)

Consumer advocates report that policyholders are confused and angry, which tracks. Although the expiration date was well known in policy circles — you know, the circles most Americans don’t travel in — there was no large-scale federal outreach campaign warning consumers about the impending sticker shock.

“People budget around their monthly premium,” explained a health policy analyst, stating the obvious. “When the increase shows up without warning, it feels like the rug has been pulled out from under them.”

Insurers did send notices, of course, but those were written in the traditional technical insurance language that requires a law degree and a Rosetta Stone to decipher.

The Political Blame Game Begins

Democrats are thrilled — or at least as thrilled as one can be about millions of people losing affordable health care — because they finally have a concrete campaign issue voters will feel in their bank accounts immediately.

“The public now gets that the subsidies are what’s keeping health care costs down,” Rep. Ami Bera told Politico, presumably with a straight face. “I think the public’s angry. So I think they will blame the party in charge.”

Democrats have spent months laying groundwork for this moment, viewing health care as a proven voter motivator ever since Republican attempts to dismantle Obamacare helped fuel Democratic gains in the 2018 midterms. The strategy even shaped last fall’s government funding showdown, which resulted in a record 43-day shutdown. Senate Democrats ultimately agreed to reopen the government without extending the subsidies, but many believe the prolonged fight elevated the issue heading into the midterms.

Republicans, meanwhile, have struggled to settle on a unified response beyond “this is fine, actually.” President Trump has called concerns about rising costs a “hoax” promoted by Democrats and the media, pointing instead to economic growth metrics that don’t help when your premium just tripled.

GOP leaders have criticized the subsidies as wasteful and vulnerable to fraud, noting they benefit some higher-income households. They have not, however, rallied around an alternative plan that would provide immediate relief. Instead, they’re banking on last year’s tax cuts — which conveniently began taking effect this year — to carry them through the midterms.

A Kaiser Family Foundation poll from December found that roughly three-quarters of marketplace enrollees would blame Trump or Republicans in Congress if the subsidies lapsed. Fortunately for Republicans, polls are just numbers until people actually vote.

What Happens Now?

Without renewed subsidies, experts warn that healthier and younger enrollees will likely drop coverage, deciding they can’t justify the higher costs. This will shrink the risk pools, which could drive premiums even higher in future years for those who remain. It’s a doom spiral, but make it health insurance.

Congress could still act to restore or replace the enhanced subsidies. This would require bipartisan agreement, which historically happens roughly as often as Halley’s Comet appears — and is about as predictable.

In the meantime, enrollment counselors are urging consumers to shop carefully during open enrollment, compare plans, and check whether changes in income or household size might restore some eligibility for assistance.

Translation: good luck out there.