The Trump Era has successfully protected consumers from consumer protectors

The CFPB and other pro-consumer agencies have been defanged and it's open season on the rest of us

President Trump has shifted his attention to his legacy in recent weeks and, other than the Iran War, seems most focused on the imperial gateway to Washington he hopes to build along the Potomac and on the grand ballroom he envisions where the White House East Wing used to be.

But there’s one group that can’t say Trump didn’t attend to their needs — consumers. Unfortunately, Trump’s idea of consumer protection is protecting them from the agencies that once worked on their behalf, thus abandoning them to the banks, fintech sharks and insurance companies that had been at least partially tamed during previous administrations.

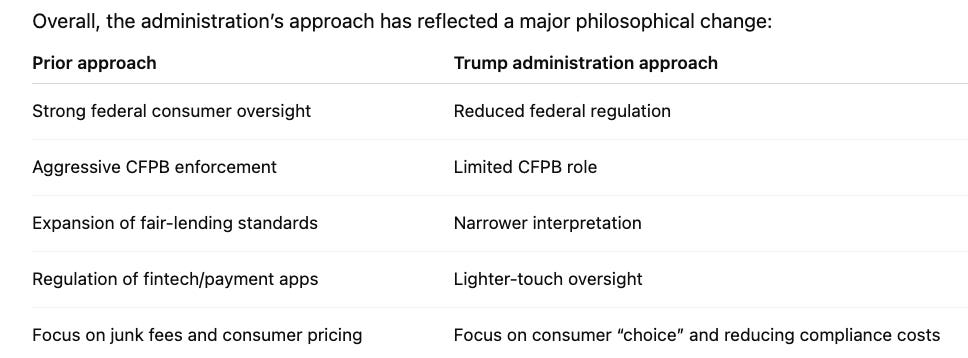

To put it in plain language: The biggest consumer-protection changes under the second Trump administration have centered on weakening or reversing federal oversight — especially by the Consumer Financial Protection Bureau (CFPB) — while shifting more responsibility to states and private lawsuits, which at best can mount a haphazard effort.

Big money is at stake and corporations are ready to pony up when they see a chance of slicing a bit more off your net worth. That means political contributions, a blight on democracy, and lobbying, which is breaking new records under this White House.

Here are some of the highlights:

1. Scaling back the CFPB

The most significant change has been the administration’s effort to dramatically reduce the power, staffing, enforcement activity, and even long-term viability of the CFPB, the agency created after the 2008 financial crisis to police consumer financial abuses.

Key actions include:

Halting or slowing investigations and enforcement actions;

Attempting major staff reductions;

Dropping or settling some pending cases;

Suspending vital supervisory activities; and

Challenging the bureau’s funding structure in court.

Critics say this leaves consumers more exposed to abusive lending, junk fees, and fraud. Trump supporters and lobbyists for the affected industries argue the CFPB had become overly aggressive and burdensome to banks and fintech firms, which had cried out piteously for rescue.

2. Repeal of the overdraft fee rule

Trump’s team axed a CFPB rule that would have capped many overdraft fees at $5 for large banks.

The Biden-era rule was projected to save consumers billions annually by limiting high overdraft charges. Banks argued with a straight face that the rule would reduce access to overdraft services — by which they meant they would stop covering overdrafts if they couldn’t continue charging $25 or more for each one — thereby pushing consumers toward worse alternatives, like payday loans and various fintech schemes.

This rollback is one of the clearest examples of the administration reversing “junk fee” regulation, proving once again that junk, like beauty, is in the eye of the beholder.

3. Rollback of oversight for payment apps and digital wallets

The administration’s minions also abolished a CFPB rule that would have subjected large payment platforms — such as digital wallets and peer-to-peer payment apps — to stronger federal supervision similar to banks.

That affects oversight of:

Digital wallets;

Peer-to-peer payment systems;

Some fintech firms; and

Big-tech financial services.

Supporters of the repeal said the rule was “regulatory overreach.” Critics warned it reduced fraud and privacy protections in rapidly growing payment systems.

4. Narrowing fair-lending and discrimination standards

The administration has moved to weaken how anti-discrimination laws apply in lending. A proposed CFPB rule would largely eliminate “disparate impact” enforcement — the idea that lenders can violate fair-lending laws even without openly discriminatory intent if policies disproportionately harm minorities or women.

If finalized, this would:

Make fair-lending enforcement narrower;

Reduce compliance burdens on lenders; and

Make it harder to challenge discriminatory lending patterns.

Consumer advocates and civil-rights groups strongly oppose the change.

5. Reduced emphasis on “junk fees”

Several Biden-era efforts targeting:

credit-card late fees;

overdraft fees;

surprise charges; and

restrictive contract clauses

have been delayed, challenged, repealed, or deprioritized.

Industry mouthpieces argue these rules interfered with pricing flexibility and innovation. Consumer groups say they would have saved households billions of dollars annually.

6. Slower movement on medical debt protections

The CFPB had pursued rules to:

remove medical debt from credit reports;

restrict debt-collection practices; and

strengthen contract rights for consumers.

Many of these initiatives have stalled or faced repeal efforts under the Trump administration.

This is particularly important because medical debt remains one of the largest sources of damaged consumer credit and bankruptcy.

7. More industry-friendly approach to fintech and banking

The administration has generally taken a more permissive approach toward:

digital payment systems;

bank partnerships; and

regulatory “sandboxes.”

The philosophy has been:

less federal intervention;

more innovation;

lighter compliance burdens; and

greater reliance on market competition.

Critics argue that lighter oversight increases fraud, data harvesting, predatory lending, and privacy risks.

8. Greater reliance on state attorneys general

As federal enforcement has weakened, state attorneys general — especially in states like California and New York — have increasingly filled the gap with their own lawsuits and regulations. So-called “red” states generally spend their resources on social issues and leave consumers to look out for themselves.

This means consumer protections are becoming more uneven nationally:

stronger in some states;

weaker in others.

The broader policy shift

Supporters say these changes:

reduce regulatory burdens,

encourage innovation,

lower compliance costs,

and expand financial options.

Critics argue they:

weaken protections against predatory practices,

reduce accountability,

and shift more financial risk onto consumers.

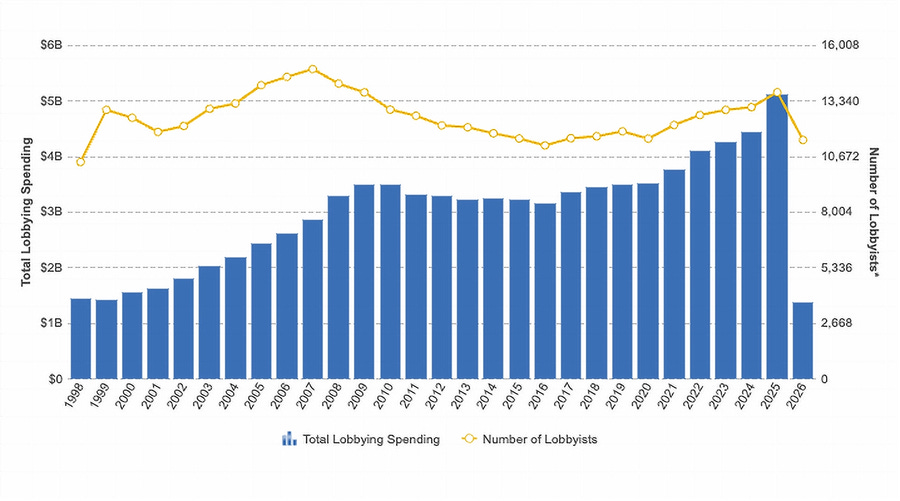

Quick: What’s the biggest growth industry in Washington?

The promise of all this deregulations is that it supposedly reduces paperwork and helps bankers sleep better at night. Perhaps but for whatever reason, companies are eager to get their share of the new relaxed approach to consumer protection.

They do that in the time-honored American way — by hiring lobbyists to woo the White House, Congress and the regulatory agencies. And sure enough, spending on federal lobbying appears to have increased significantly during both Donald Trump’s first term and especially during his second administration.

Total federal lobbying spending reportedly topped roughly $5 billion in 2025, up about 14% from 2024 and the highest level ever recorded under modern disclosure rules. This funding free-for-all is fueled by battles over taxes, trade policy, healthcare, tariffs, and AI rules.

Industries facing major regulatory changes — including tobacco, artificial intelligence, higher education, energy, crypto, and healthcare — sharply increased lobbying activity, Reuters reported.

Research universities alone boosted federal lobbying spending from about $28 million in 2024 to more than $37 million in 2025 as they reacted to proposed funding cuts and policy shifts, according to Inside Higher Ed.

AI companies that barely had Washington operations a few years ago are now spending millions quarterly on lobbying tied to copyright, export controls, cybersecurity, and regulation, per Axios.

Historically, lobbying also increased during Trump’s first administration. Analyses from groups including OpenSecrets and Statista found both the number of registered lobbyists and overall lobbying expenditures rose between 2017 and 2021, despite Trump’s campaign pledge to “drain the swamp,” according to Statista.

Why the increase?

In general, Washington lobbying spending tends to rise whenever businesses believe major federal policy changes could strongly affect profits or regulation — and Trump’s administrations, particularly the current one, have created a high-uncertainty environment that encourages more lobbying, not less.

The psychology behind this madcap spending is clear: Companies are reluctant to spend too freely when they face a White House and Congress that are trying to at least look like they give a damn about their constituents. When the gates are thrown open, as in the current climate, a land-rush mentality takes over and it’s a seller’s market for influence peddlers, “strategists” and out-of-work politicians, who are highly prized by lobbying firms.

Big bucks, for nothing

And what does all this frantic jockeying for power get for Americans looking for help with education, healthcare, infrastructure, consumer protection and other socially beneficial programs?

Good question, especially when you consider how much is spent on election campaigns. The total raised by all 2024 presidential candidates was about $1.87 billion, per OpenSecrets — notably lower than 2020’s $3.98 billion, partly because Biden’s pre-July fundraising rolled into Harris’s operation rather than starting fresh.

So round up spending on federal lobbying and the presidential campaign and you have $7 billion that produced nothing of value but could have been spent on something worthwhile or simply not spent at all.

Oh, and don’t forget: the federal deregulation that got underway in the Reagan years returned a lot of regulatory power to the states, resulting in hefty spending on political campaigns at the state level and — you guessed it — lobbying.

A final slight digression: the author spent a few years in a D.C. lobbying firm commonly described as a “powerhouse.” We had a startlingly large conference room with a table that easily seated 40. We would gather there to hold meetings where our corporate clients’ needs were supposedly discussed and analyzed, each of us billing a very healthy hourly rate and producing nothing of any particular value.

I always thought this was basically consumer fraud, except that in this case, the consumers were huge corporations that sought every opportunity to throw money at their problems in hopes of eradicating them, or at least giving them someone to blame when things went south.

Want to drain the swamp, return power to the people, make government more responsive and so forth? Provide public funding of campaigns and outlaw campaign contributions.