The U.S. owes more than it makes. Here's what that means for your wallet

The national debt has now surpassed the size of the entire U.S. economy. The effects are already showing up in your mortgage, your credit card bill, and your retirement.

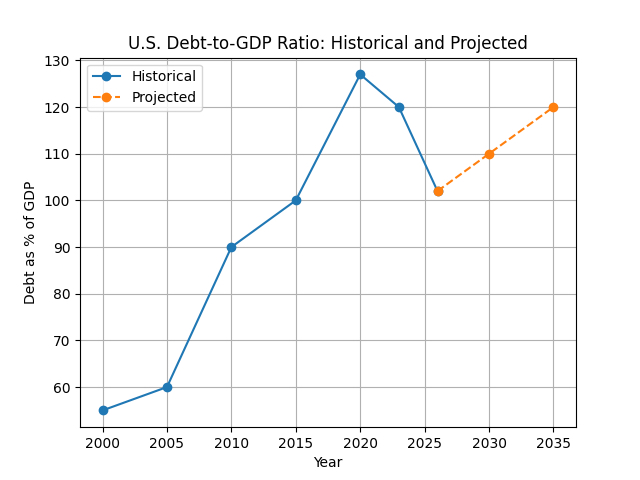

The number is almost too big to picture: the United States government now owes more money than the entire country produces in a year. The debt-to-GDP ratio — Washington’s tab measured against the economy’s output — has crossed 100 percent, a threshold that once seemed unthinkable and now seems permanent.

It doesn’t mean the country is going broke. It doesn’t mean your personal finances are suddenly on the hook. And it almost certainly doesn’t mean a crisis is arriving next week. What it does mean is quieter, slower, and in some ways harder to fight: a steady erosion of financial flexibility — for the government, and through it, for ordinary Americans.

“The impact is gradual, not sudden,” said one economist. “But gradual doesn’t mean painless.”

The bill is already in your mailbox

The most direct effect on consumers isn’t some future reckoning — it’s the borrowing costs they’re paying right now. When the federal government needs to finance its debt, it issues Treasury bonds. More bonds mean more competition for capital, which pushes interest rates higher across the economy. Those rates don’t stay on Wall Street.

They show up in the 7 percent mortgage that priced a first-time buyer out of their neighborhood. In the credit card balance that compounds faster than a family can pay it down. In the auto loan that turned a $35,000 car into a five-year financial commitment.

Interest rates are shaped by many forces — Federal Reserve policy chief among them — but the sheer scale of federal borrowing acts as a persistent floor, making it harder for rates to fall and easier for them to stay elevated.

The tax and benefits squeeze is coming

The arithmetic of debt service is unforgiving. The federal government now spends more on interest payments than on national defense — money that is not building roads, funding research, or keeping Medicare solvent. As that share of the budget grows, policymakers face a narrowing set of options: raise taxes, cut spending, or some combination of both.

That eventually means one of several things. Higher income or payroll taxes. Reduced deductions. Trimmed benefits. Social Security and Medicare, already under long-term fiscal pressure, become even harder to protect when a growing slice of every budget goes to bondholders before it reaches beneficiaries.

None of this happens overnight. But the direction of travel is not ambiguous.

The cushion is thinner than it used to be

When the 2008 financial crisis hit, Washington spent aggressively to cushion the blow. When COVID arrived in 2020, Congress deployed trillions in stimulus with unusual speed. Both responses were possible, in part, because the U.S. had accumulated less debt relative to its economy and retained more credibility with bond markets.

That cushion is thinner now. A future recession, a major geopolitical emergency, a financial shock — any of these will test a government that has less room to maneuver than it did a decade ago. Smaller stimulus. Slower response. More political gridlock over the price tag.

Why the sky hasn’t fallen — and may not

It is worth saying plainly what the debt milestone does not mean. Japan has run a debt-to-GDP ratio above 200 percent for years without a financial collapse. The United States issues the world’s reserve currency and enjoys deep, global demand for its Treasury bonds — advantages no other country fully shares. A default under normal conditions remains essentially unthinkable.

The genuine risk isn’t a sudden crash. It’s a slow drift: higher baseline borrowing costs, less generous public programs, less margin for error when things go wrong. Countries don’t usually go broke — they gradually become less able to do the things they once did.

What to do now

For households thinking practically rather than politically, the implications point toward a few concrete moves: lock in lower interest rates when the opportunity arises, attack high-interest debt with urgency, and build more financial flexibility into budgets that have long assumed a government ready to step in during hard times.

The debt clock keeps running. The effects arrive not as a thunderclap but as a slow tightening — in loan rates, in tax bills, in benefit checks, in the diminished capacity of a heavily indebted government to catch its citizens when they fall.

While it’s true that no individual consumer can do anything about the big picture, it’s also true that nearly everyone can take a careful look at their household spending and find a way to build in a little cushion to create a bit of what engineers call “headroom.”