Welcome to the superhighway of fraud

Consumer fraud reports up more than 6 million since 2001

Back around the turn of the century, folks still talked about the Information Superhighway, a somewhat fanciful name for a universal broadband network. That was when everyone thought the internet would grease the skids of knowledge, encourage learning, and enhance commerce.

It has perhaps done a few of those things but mostly it has contributed to the formation of new ways to separate consumers from their privacy and money. It has spawned entirely new types of thuggery that are piously described as innovation, things like Search Engine Optimization, the holy grail of online chicanery. It’s the “science” of publishing keywords (“extended warranty,” “guaranteed weight loss,” “walk-in bathtub”) and plugging in just enough random text to make them look like actual information. This, in turn, makes it difficult to find anything that is actually written for the purpose of conveying useful information.

What gets lost in this welter of misinformation and patent medicine chicanery, besides common decency, is the recognition of certain very obvious facts — for example, that consumer fraud and financial fraud are just different ways of describing theft.

People who would not think of donning a mask and gun to stage a bank robbery think nothing of manipulating consumers to invest in pyramid schemes, buy trashy consumer goods or surrender their life savings to someone pretending to be the FBI.

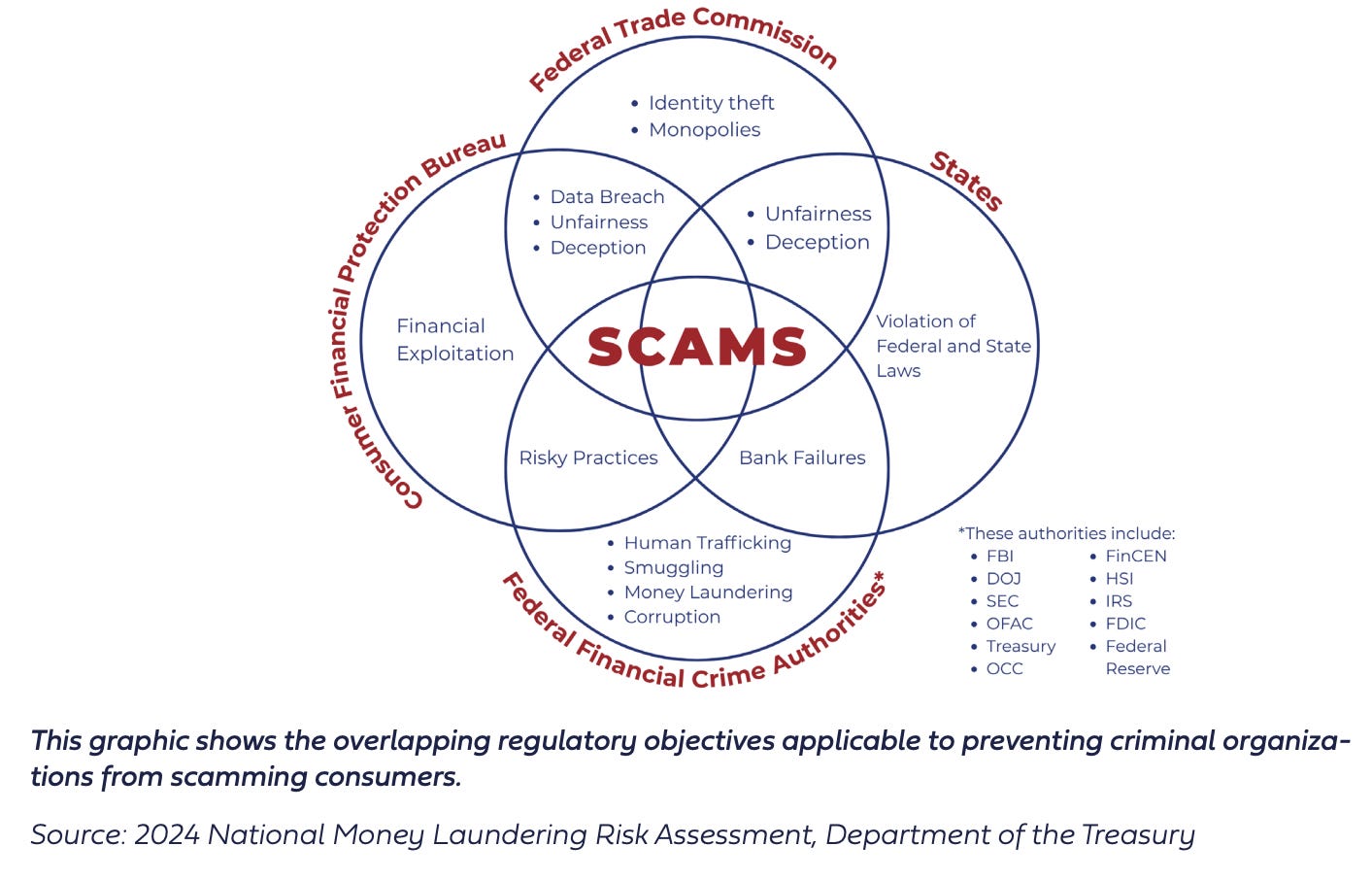

Consumer fraud is theft. Plain and simple. The Consumer Federation of America (CFA) recognizes this perhaps startling fact in a new paper, Follow the Money: Bridging Consumer Protection and Illicit Finance to Stop Scams. It looks at the dramatic rise in fraud and calls for closer coordination between consumer protection and the policing of illicit finance.

6 million more fraud reports

The paper notes that fraud reports to the Federal Trade Commission have surged from just over 325,000 in 2001 to approximately 6.5 million in 2024, reflecting how advances in technology and AI have made scams more pervasive, scalable, and financially devastating.

The analysis finds that while scams take many forms, they all end the same way: by tricking victims into sending money.

Over the past two decades, the traditional boundary between illicit financial activity and consumer fraud has eroded, as criminal networks increasingly rely on mainstream financial institutions, payment apps, and digital banking tools to move stolen funds.

Despite this convergence, the regulatory systems responsible for policing illicit finance and protecting consumers remain largely “siloed.” CFA argues that this separation no longer reflects how modern scams operate and leaves consumers exposed to systemic failures.

The paper calls on policymakers and financial regulators to close this gap by aligning supervision and enforcement so that efforts to combat money laundering and illicit finance also deliver direct relief to scam victims.

It emphasizes that scams are both a financial crime and a consumer protection issue, and warns that as digital payments continue to expand, consumers will increasingly bear the costs of institutional compliance failures unless safeguards are strengthened.

CFA concludes that regulators must adapt their oversight to ensure innovation does not come at the expense of consumer safety, financial security, and trust in the banking system.

That’s a worthy goal but one that will be hard to accomplish in an era of rampant deregulation and unmatched corruption. The Trump administration has virtually abolished the Consumer Financial Protection Bureau and many state attorneys general — traditional champions of the consumer — now devote their energies to suing other states and the federal government, leaving consumers to fend for themselves.

Instead of a superhighway, it’s a very expensive toll road.